IN the first major policy announcement since formation of the coalition government the stimulus package was announced on July 23rd 2020. It is the next step in recovery for businesses following the introduction of the previous wage subsidy scheme.

The estimated cost of €7.4 billion represents the government’s commitment to Irish businesses and includes a mixture of tax cuts, expenditure and support credits. The stimulus package represents a light at the end of the tunnel for many businesses and it includes a number of legislative changes as well as Revenue precedents with the aim of assisting businesses return to a new normal. The government has introduced €1 billion of taxation measures to assist the recovery so, with this in mind we have highlighted some of the opportunities arising from a tax perspective for equine trades as businesses respond to the ever changing working environment.

Following legislative change, sole traders and partnerships have the temporary opportunity to utilise losses arising in 2020 against their 2019 income. The stimulus package includes additional income tax reliefs available as follows:

Laura is a breeder who trades as a sole trader. For the year of assessment 2019, Laura earned taxable profits of €80,000. Laura anticipates for 2020 she will have difficulties selling stock and that this will lead to a loss of €15,000. She also has excess capital allowances of €5,000 on her farm buildings. Laura is single, entitled to standard tax credits and has no preliminary tax paid for 2019.

Income taxpayers are obliged to pay preliminary tax of either:

- 100% of the prior year liability, i.e. 2019 liability when making payment for 2020, or

- 90% of the estimated current year liability, i.e. 2020

Laura can further reduce her payment requirements in the above example by €20,411 as she anticipates a loss for 2020 and as such no taxable profits arise based on her estimates for 2020. By planning and reviewing the stimulus package Laura has saved €36,411.

Further to the above, a temporary corporation tax loss relief measure was introduced in the Financial Provisions Act 2020. If during the specified accounting period (any accounting period of a company carrying on a trade which includes some or all of the period commencing on March 1st 2020 and ending on December 31st 2020), a company has estimated losses, then subject to satisfying certain conditions, an interim claim can be made to use 50% of those losses against 2019 profits.

debt warehousing

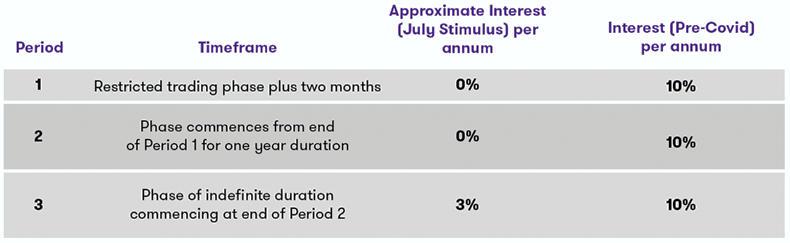

THE Government passed legislation which allows for the deferral or ‘warehousing’ of VAT and PAYE liabilities for SME’s and larger groups on application basis.

The July Stimulus package allows businesses which have been negatively impacted by Covid-19 to defer unpaid VAT and PAYE for a period of 12 months from the date which the business resumes trading. The periods covered by this scheme are from the date the business was unable to trade due to Covid-19 and for a further two months after the business reopens.

The scheme is divided into three distinct periods.

As numerous equine trades qualify as flat rate farmers, these businesses will not be impacted by the option to defer VAT payments. However, the above presents an opportunity to plan cash flow and delay payment of liabilities without the implication of interest on non-payment of taxes particularly for equine businesses with employees.

Your advisors should be aware of the above and particularly where other debts are arising, you should query if the above is an option which is available and which could benefit your business.

The reduction in annual interest charge on income tax and corporation tax for late filing/payment is another point which should be considered by your advisors.

Interest on overdue income and corporation tax can be reduced to 3% as noted above where an agreement is in place before September 30th.