THE major yearling sales have generated headlines about record prices, seven-figured transactions, and high percentages of lots being sold, but the wider picture has been far from rosy, and it is the foal sales of the next few weeks that will supply many yearling slots for 2019.

As has become the norm, many represent young, unproven stallions who have large numbers on offer, adding to the challenge many face in trying to sell or pinhook a foal.

Memories of the second-crop sires may have dulled slightly, and the fate of those with their third may hinge on how their two-year-olds performed on the track, even if the stallion is a classic or middle-distance type rather than one with realistic prospects of being a progenitor of precocity.

If your horse is one of 80, 90, 100 or more by the sire this year then it is at risk of getting lost in the crowd. Minor flaws that the rarer specimen possesses become value-slashers, and if he was a lesser light of his racing days or is producing less than supermodels, then that hill to climb becomes a mountain.

There may be some tremendous bargains found, just as there are every year – the yearling whose price dwarfs his foal tag, the juvenile whose pre-sale breeze adds noughts to the end of his yearling price.

But producing horses that are destined for or fall to the bottom of the market is a recipe for disaster, and there will likely be some difficult times and choices to be made in the coming weeks and months.

This week’s Goffs Autumn Yearling Sale, for example, saw a clearance rate of just 59.5% from 504 offered, an average price of €5,473 and a median of only €3,000.

So what lies ahead? And can the recent past inform?

A total of 410 stallions were represented by at least one yearling sold in Europe in the first 10 months of this year, and 318 had at least one foal sold in 2017, but many had very small numbers change hands. The first step, therefore, towards investigating how those foal sales link to the 2018 yearling ones was to ignore all stallions who had fewer than 10 in each category, which left a total of 82 sires.

Why?

Just one good sale can skew an average considerably, and that is not useful. A higher cut-off point would be ideal but leave too small a dataset, and using the median would be even better, but averages are what tend to be quoted, so that’s what was used.

By setting this cut-off point, some notable stallions were eliminated. Dark Angel (88), Kingman (42), Invincible Spirit (39), Oasis Dream (37), Galileo (35), Frankel (26), Fastnet Rock (22), Pivotal (22), Dubawi (20), Kitten’s Joy (16), Shamardal (15), and Dansili (14) all had more than enough yearlings to make it through, but only had between one to nine foals sold in 2017.

Although this may seem like a lot of valuable data was discarded, that group’s prices are not really reflective of the typical sales horse.

They represent the elite end of the market and their strings of high six-figure and even the occasional seven-figure lot pull the overall average upwards.

Besides, you don’t change your eligibility criteria just because you’d like to add someone else in.

This colt by Gleneagles was sold by Newsells Park Stud at the 2018 Goffs UK Premier Yearling Sale for a record £380,000. Photo Sara Farnsworth

Four National Hunt stallions were also removed: Kayf Tara, Ocovango, Sageburg, and Soldier Of Fortune. Why? Those pinhooked foals are usually reoffered as stores, and not as yearlings, and returns for the National Hunt yearling sales tend to be lower than for the sector’s foal ones, a pattern that their data reflected.

The remaining 78 got an additional variable: a crop code – with one representing first crop, two for second crop, three for third crop, and four for all other stallions.

There remained a total of 1,665 foals and 3,666 yearlings, with overall average prices of €35,083 and €55,558 respectively. See Table 1 for the breakdown by their crop category.

How many stallions achieved a better than the overall average price for their foals (€35,083) and for their yearlings (€55,558) in the period under review?

The answers are 26 and 25. So, 52 and 53 sires respectively – representing a total of 1,196 (67.7%) foals and 2290 (62.5%) yearlings – failed to reach that target, giving an excellent illustration of how misleading averages can be when trying to make any sort of prediction about what you might be able to expect for your horse at the sales.

Of course, stallions who have outstanding results with one or several offspring can see their average brought down by a few lesser lights, just as a high achiever’s excellent returns can be misleading.

A stallion could have a dozen sold, with one monster price leading to an average that surpasses what each of his other 11 made.

He could have had 20 who failed to change hands at all, but they’re not included in his figures, whereas the lower-ranked sire with the same number offered could have had all 32 sell at a fairly consistent level.

Which was the real success story?

And if one took a view that, say, €100,000 is an unattainable goal by most and so chose to conduct an analysis with only those who were sold for less than that, then you would see a very different picture of the state of the market.

The elite prices have a masking effect.

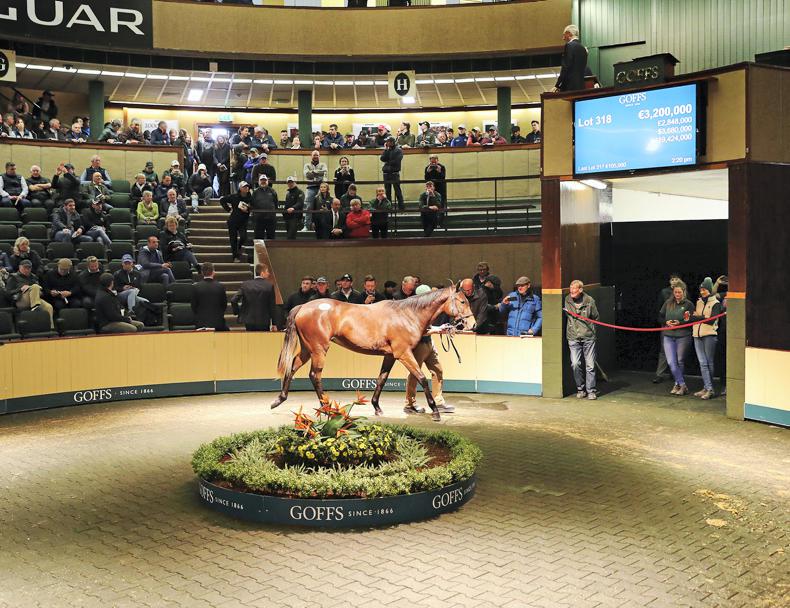

Galileo filly ex Green Room from Ballylinch Stud made €3,200,000 sold to Phoenix Thoroughbreds at the Goffs Orby Sale. Photo carolinenorris.ie

So, how did the bottom end look?

From the lowest returns, there were 21 whose 411 (24.7%) foals failed to average even €15,000 – of whom five (184; 11.1%) didn’t even hit half that much – and 26 whose 992 (27.1%) yearlings averaged less than €20,000, of whom six (148 lots; 4%) didn’t even reach a mean of €10,000.

That is sobering. That is financially inviable. That is cold reality.

When these were looked at by the crop grouping, something was immediately apparent.

Despite the rush by many to use stallions in their first year, only five of the 20 beat the average foal price in 2017, which means that three-quarters of those stallions did not. Of the five, four were multiple Group 1 winners, the other one a dual Group 2 scorer.

Only two were second-crop sires, two were third-crop sires (so had two-year-olds on the track that year, which can be influential), and the other 11 were all more established.

In percentages, that’s 22.2% of the second-crop sires covered by the data, 20% of the third-crop sires, and 28.2% of the established sires.

I did not run any inferential statistical analyses, although I doubt there is any significance in the differences between those proportions.

There are, of course, members of those groups who were eliminated due to lack of numbers, so those figures are not reflective of the entire cohorts anyway.

How did those first-crop sires fare at their first yearling sales?

Only those same four multiple Group 1 stars beat the €55,558 average (20%). The same two second-crop sires plus one more achieved the feat (33.3%), as did three third-crop sires (one from the top end of the foal data) (30%), and the other 15 (38.5%) were in the established category.

It would seem that if a first-crop stallion does particularly well at the foal sales then he will repeat the feat at the yearling sales.

Of course, not only is that something that we’ve all observed so many times before, and has a strong ‘duh factor’ about it, but it is not a claim of prediction or certainty that can be made based on such a cursory analysis.

Another striking facet of the results for first-crop sires was that, unlike all of the other groups – each of whom showed a low five-figured increase (significance not calculated) – there was almost no difference between the overall average price their stock made as foals compared to their overall yearling average – €43,119 versus €44,775, despite having almost twice as many sold in the older group.

There could be something in this, but can we draw any conclusions? No.

As with all of the groups, varying numbers of their yearlings were also offered as foals – sold or otherwise – but it would take a far more detailed analysis, looking closely at each individual sire over crops-worth of returns, overall market trends, perhaps including breeze-up sales, and then applying inferential statistics to be able to use results as a means for prediction with any degree of accuracy.

What the analysis here does show is a black-and-white snapshot of the current state of the market, an environment that many know all too well is a very difficult place.

If you have an elite-bred foal or yearling, minus unattractive flaws, then the rewards can be great, but the majority can but dream of playing at that level.

For them, there are tough decisions to be made, mares and stallions to be re-evaluated for possible export or retirement, and what to do with the large numbers who never made it even into the unrefined datasets – the many foals and yearlings who failed to find a buyer.